Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Welcome to Trade Secrets. Last week, following the meeting of EU member states two weeks ago on dealing with China, trade commissioner Maroš Šefčovič met his Chinese counterpart Wang Wentao. The outcome? A promise to address the trade issues including the deficit in some vaguely specified way by October. In a column just before that EU meeting I reported on a war-gaming exercise I’d taken part in on a trade showdown between the EU and China. And how did it end? China comprehensively won and gave nothing more than a woolly promise for a plan in two months’ time. (I’m not talking my book here: I was on the team playing the European Commission.) Uncanny. I strongly predict nothing substantive will happen in October either. Today’s main pieces are on the return of pharmaceuticals pricing as a US trade priority and the USMCA imbroglio. Charted Waters, where I look at the data behind world trade, is on European stock prices.

Me and the pharma

(It’s a song.) Time was when pharmaceutical pricing was right up in the top three or five at least of contentious topics whenever the US tried to close a trade deal. Some may forget this, but the Asia-Pacific CPTPP deal (then just “TPP”) stalled in Congress in 2015-16 before Donald Trump killed America’s participation in 2017. One big reason was a dispute over how long the creators of biologic drugs could retain clinical trial data to prevent biosimilar versions being made.

Under Joe Biden, thanks to his administration’s affinity with campaign groups such as Public Citizen, sworn enemies of the pharma industry, the slavish support eased off. His administration even pretended to support a move to waive patents for Covid-19 vaccines at the WTO before it became clear it was just for show.

Anyway, pharma’s back, and Trump has a plan to push up drug prices abroad to compensate companies for driving them down in the US. This is going to be a nice little test of foreign governments’ ability to resist him and particularly their ability to act collectively. He’s started a Section 301 unfair trade investigation of Germany, which boldly decided this was a good time to launch a new procurement policy pushing drug prices down, a pretty gutsy thing to do for a country with its own big pharma industry. The EU doesn’t have a bloc-wide pricing or procurement policy — developing the Covid vaccine involved breaking a lot of new ground — but a bunch of smaller EU countries including Belgium, the Netherlands and Ireland have got together and sounded the bugles of defiance across the Atlantic.

Who knows how this will end up, but it looks like the right negotiating strategy at least. Get out in public saying what you’re going to do and act in concert with others if you can, which makes it politically easier to resist pressure.

Or you could do what the UK has done, which is to succumb to a pincer movement of lobbying like a gang of absolute amateurs. On one side, the pharma companies threatened to disinvest from Britain if prices didn’t rise. On the other, the US administration forced Sir Keir Starmer’s government under pain of tariffs to agree to raise domestic prices in one of those absurd trade deals written on a metaphorical napkin while being threatened by a figurative gunboat.

This commitment could have a serious impact on drug availability and public health. As David Henig of the ECIPE think-tank correctly points out in a good thread here, this is exactly what you get when you make trade policy in secret. You can’t use public opinion as an excuse to reject foreign governments’ demands (“we couldn’t get this through if we wanted to, just look at the demos in the streets”). Instead you’re left feebly trying to hope the voters and parliament don’t notice. The UK government now claims it was always a brilliant strategy to strengthen pharma production in Britain, strongly reminiscent of when my cat falls off a sofa and pretends she meant it all along.

It’s not as if they weren’t forewarned. Here I am writing about the threat twelve years ago. The lack of outcry in Britain is quite striking. There were big protests in the UK in the mid-2010s about the much more theoretical threat to the NHS from the abortive transatlantic TTIP trade deal, which supposedly would force the UK to accept private US healthcare providers. Maybe the health unions felt threatened by that in a way they don’t by drug prices. Anyway, for any government wondering how to deal with the Trump pharma threats, don’t do what the UK did.

It’s fun to stay in the USMCA

(It’s a song.) My contention that the Trump trade policy is largely a job creation scheme for trade negotiators, journalists and consultants got another boost last week when the US announced that it wouldn’t be extending the USMCA trade deal aka CUSMA, ACEUM — my favourite name for some reason — and T-MEC.

Simon Lester of World Trade Law sets out exactly what that means. It’s not that the deal is dead, nor that it’s necessarily automatically going to expire, but that the Trump administration wants to force changes in it before agreeing to extend.

The statement from US trade representative Jamieson Greer reiterated one of the administration’s main concerns, the deficit it runs with both partners. In the past it has (relatedly) complained that too much of the supply chain, particularly for autos, is located in the US, suggesting that rules of origin need to be tightened once again, and about labour standards not being properly adhered to.

It’s certainly the case that the other two members want the deal to continue. As I wrote recently, whatever Canadian Prime Minister Mark Carney says about building a post-US global trading system based on the middle powers, he’s also extremely cognisant of the reality that diversifying from trade with the US will take a very long time. Canada’s minister was almost embarrassingly effusive about the deal last week. Mexico’s trade minister Marcelo Ebrard also sounded positive, though pointed out that T-MEC rules of origin were among the most stringent in the world and he couldn’t see what more they could do.

The fundamental problem is that the US wants to do things with the USMCA that are either very hard to do (I link again here to Trade Secrets favourite Desirée LeClercq’s definitive piece on the Rapid Response Mechanism, which was intended to enforce high labour standards) or outright contradictory (eliminating trade deficits with trade policy). The supply chain platform Altana, which has a contract on forced labour with US Customs and Border Protection and the Department of Homeland Security, says its panel of experts identified transshipment and the value of inputs from outside North America as the weakest parts of the deal.

In the absence of an actual plan, we have to assume that keeping it up in the air is itself tactical, perhaps using the threat of killing it as a perpetual threat to coerce Canada and Mexico into doing whatever the US wants. In the meantime, tethered though Canada and Mexico remain to the US, this creates an incentive for them to continue diversifying, with further moves on electric vehicles being an obvious area.

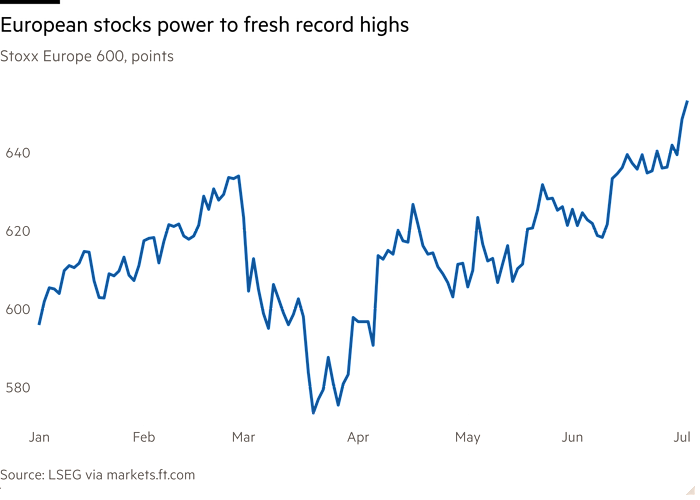

Charted waters

The resilience of US stock prices to the trade war and Trump more generally has been impressive, but in relative terms European stocks have outperformed, including in local-currency terms. To the extent the trade war has affected markets, it has hit the aggressor more than the victim.

Trade links

Bloomberg reports on China calling for unimpeded passage through the Strait of Hormuz, while chatter mounts about a toll system. You have to admit that would be very funny.

A former Biden economic adviser argues that the US cannot let China get a lead in data centres the way it did in rare earths.

The FT reports on how the EU’s smart-border system ran into trouble.

US trade historian Doug Irwin details how the US has been arguing about trade for 250 years.

The FT’s Katie Martin says the good vibes in markets mask a reset.

Trade Secrets is edited by Jonathan Moules